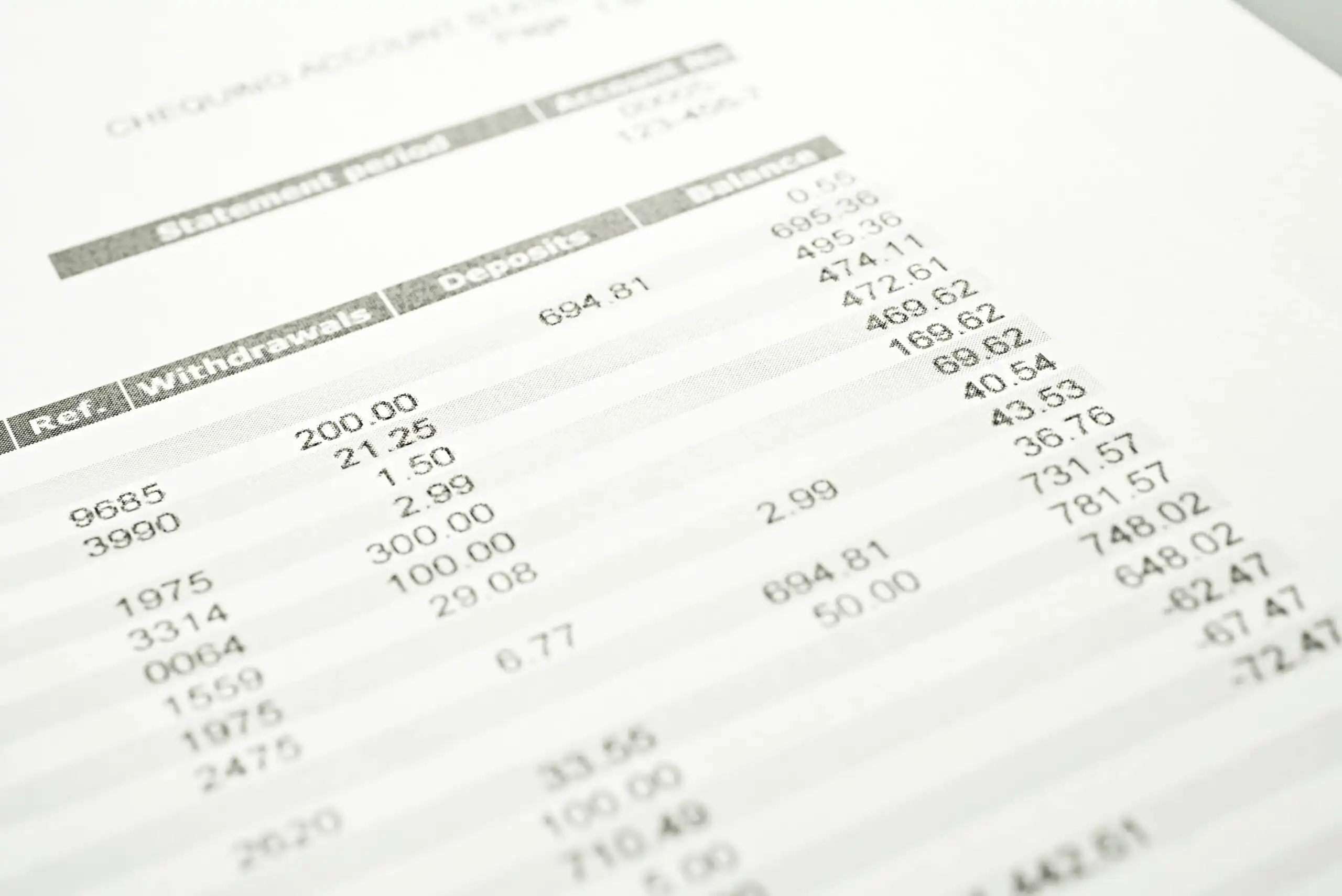

Your bank statement is a record of everything that’s happened in your bank account during a period. You can see the starting balance of the account, every activity that changed the balance, and the ending balance of the account all in one document.

Knowing how to read your bank statement gives you an opportunity to check your bank’s records for errors, which could help you avoid overcharges. It can also help you keep track of your spending habits and better manage your household finances.

How to Read Your Bank Statement

Bank statements can seem complicated, but they’re pretty simple to understand once you know what you’re looking at. You just need some basic math skills.

Account Information That’s on a Bank Statement

The first page of your bank statement will typically contain a few pieces of information, including:

- Your name and address

- The bank’s name, mailing address, and phone number

- A list of all the accounts you have at the bank (if it’s a combined statement)

- The account number or numbers for the account(s) covered in the statement

- The starting and ending dates for the statement

- The beginning balance for the account(s)

- The ending balance for the account(s)

Your statement will typically also include a quick summary of account activities, including the amount you deposited, the amount withdrawn or spent, and any interest accrued or fees charged.

How to Understand Your Bank Statement

While looking at your bank statements regularly is important, it doesn’t do much for you if you don’t understand what you’re looking at. To make sure you understand what you’re reading, follow these steps.

- Start With The Summary

Your statement should have a summary that lists the account’s starting and ending balances as well as the total of debits toward the account and credits from the account. This gives you a high-level view of the money moving in and out of the account.

- Check For Fees.

Often, the account summary will list any fees you paid during the month, so check to see if you paid any fees unexpectedly. If you did, you can find out why the bank charged the fee later and come up with a plan to avoid that fee going forward.

- Review Individual Transactions

Your bank statement contains a list of every single transaction involving that account during the statement period. That includes deposits, withdrawals, and anything else that impacts your account balance.

Each line on the statement should list the date of the transaction along with a description, whether it was a debit or credit, the size of the transaction, and the account’s balance after the transaction.

- Look For Errors

While reviewing the individual transactions, look for purchases you don’t recognize. If you notice one, take note of it so you can investigate it or report it to the bank as a mistake.

- Identify Spending Patterns

While looking over your bank statements, you might notice certain patterns in your spending. You can take note of these patterns and consider trying to change them in the future.

If you’re reviewing your account statement to try to identify spending patterns, review multiple consecutive statements to see how your spending changes from month to month.

This helps you get a more accurate and consistent picture of your cash flow over longer periods of time, rather than a shorter-term view that could be distorted by large, one-time ATM withdrawals or debit card purchases.

Why You Should Review Your Bank Statements Regularly

There are many benefits to reviewing your bank statements on a regular basis.

Fight Identity Theft

First, reviewing your bank account statements regularly helps you identify fraud or identity theft. If someone gains access to your checking account, they can take your money and you might not even notice if you don’t keep a close eye on your balance.

Reviewing your monthly statements for unusual transactions makes it more likely that you’ll spot fraudulent activity and report it to your financial institution quickly.

Avoid Bank Fees

Keeping an eye on your statements can also help you identify bank fees and ultimately reduce the fees that you pay.

For example, if you see that you pay $10 in ATM withdrawal fees every statement cycle, you can start looking for ways to avoid that fee. That might mean using contactless payment apps for everyday purchases instead of cash. Or it might mean moving to a new bank altogether.

Track Your Spending

Reviewing your bank statements is also an important part of managing your financial life. If you get your paycheck direct-deposited and use your debit or credit card for most purchases, it can be easy to lose track of the total amount of money you have in your account.

When you keep close track of your income and spending, it’s much easier to build a sustainable budget and add to your savings each month.

Reading Your Bank Statement FAQs

Reviewing your bank statements regularly is a good way to keep track of your money and prevent fraud. If you still have questions about the process, we have answers.

How Do I Obtain My Bank Statement?

In the past, banks would send paper statements to their account holders in the mail. That’s still an option these days, but most banks encourage paperless statements instead. Many now charge paper statement fees for customers who don’t opt into paperless.

Typically, you can view your electronic statements by signing in to your bank’s online account portal. There should be a section of the site where you can view your bank statement online.

What Should I Do if There’s an Error on My Bank Statement?

If there’s an error on your bank statement, the first thing you should do is see if you can identify the source of the error.

Does it look like the bank accidentally credited one of your ATM withdrawals against your account multiple times? Do you see a transaction you have no memory of making? This may help you resolve the error.

Either way, you should reach out to your bank as soon as possible. Most banks put their contact information right on the statement so you can contact them easily. Speak to a support representative, let them know about the error, and provide any information you can to support why you think it’s a mistake.

It’s important to take these steps whether the error is in your favor or not. If the bank accidentally adds money to your account, you can be certain the bank will realize and take the money back at some point. If you spend money that isn’t yours, it could leave you in a bad spot when the bank realizes its mistake.

How Long Should I Keep My Bank Statements?

How long you should keep bank statements depends largely on how long you want or need to maintain your financial records.

A good rule of thumb is to hang on to your statements for at least a year in case you identify an issue and need to go back a few statements to identify the source of the problem. With online statements, you can either download them and keep them on your computer or rely on your bank to keep them accessible online.

FDIC regulations and federal law require that banks maintain records for at least five years. Many banks will keep your statements accessible online for even longer.

Final Word

Your bank statement is the final record of every transaction you make using the account. It’s important for you to review your bank statements regularly to identify errors or find patterns in your spending so you can improve your personal finance habits.

Many people use budgeting apps to keep a close eye on their bank accounts. These tools let you view all of your accounts in one place and review transactions from a single dashboard, saving you the effort of downloading and viewing multiple statements each month. They also update more frequently than once per month, making them useful for more frequent reviews of your financial activity.

Even if you’re happy with your bank account, it’s not a bad idea to add one of these tools. Or, if you prefer, you can switch to an online bank with built-in budgeting capabilities.

Editorial & Advertiser Disclosure: The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.

Related: