There’s no shortage of ways to pay someone these days, from cash and credit cards to Zelle and PayPal. It’s easy to go your whole financial life without ever coming across a money order.

But if you’re here, someone’s asked for one, so follow these directions to fill it out.

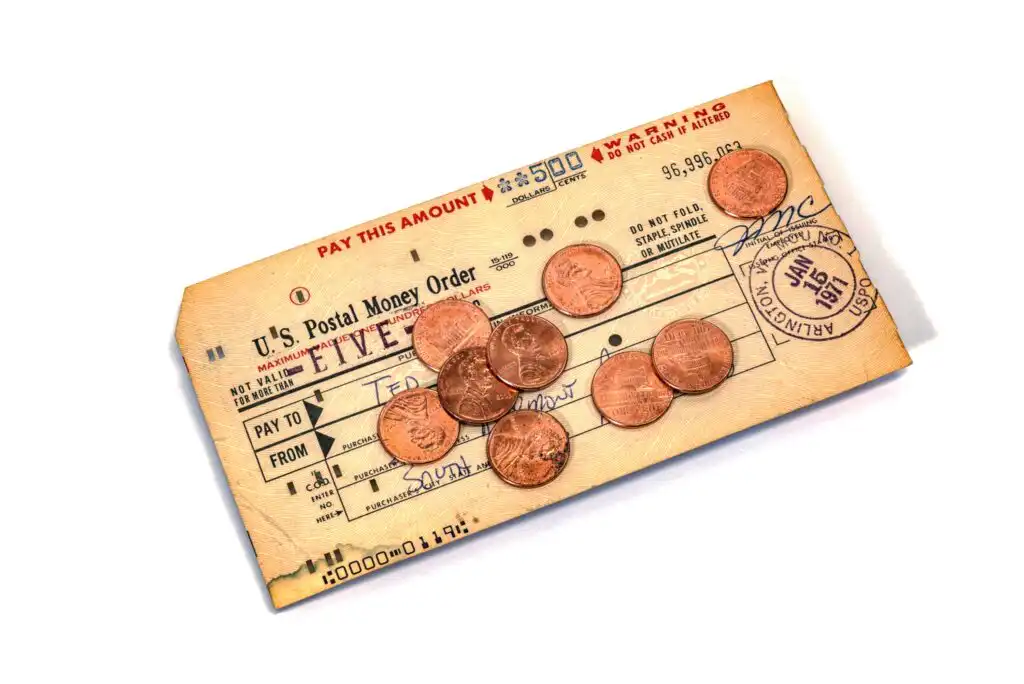

How to Fill Out a Money Order

Filling out a money order is much like writing a check. You need much of the same information, plus a little extra. Follow these steps to ensure you put all the right stuff in all the right places.

Note: Be sure you write legibly. Hard-to-read writing can make a money order invalid.

1. Provide Information to the Issuer

The company issuing the money order will fill in some information when they give you the order:

- Serial number, which identifies and tracks the money order

- Date issued

- Issuer information, such as store ID, post office number, and clerk ID

- Dollar amount up to a set limit (typically, $1,000). If you need to send a higher amount, you must get multiple money orders.

You’ll need to provide a valid ID, such as a driver’s license or passport, to verify your identity.

2. Write the Recipient’s Name & Address

Write the name of the person you’re paying on the “Pay to” line. (For some issuers, this line may say “Pay to the order of” or “Payee.”) If you’re paying an individual, use their legal name. If you’re paying a business, use the business’s name. Under that, write the payee’s address.

Should you need to send a money order to two people, be careful with your wording. If you join the names with the word “or” (e.g., Jane Doe or John Doe), either recipient can cash the money order without the other’s signature.

If you join the names with the word “and” (e.g., Jane Doe and John Doe) or don’t use a conjunction (e.g., Jane Doe, John Doe), both recipients must endorse the money order to cash it.

3. Write Your Name & Address

On the “From” line, write your legal name. (For some issuers, this line may say “Purchaser” instead.) Below that, write your address.

4. Fill in the Memo Line

The “Memo” line is where you identify what the payment is for. This makes it easier for the recipient to apply your payment correctly. Examples of notes you might include are:

- The item or service you’re paying for (e.g., “Rent, Jan. 2023”)

- Your billing account number

- The order number

5. Sign Your Name

Depending on the issuer, your money order may have a signature line. If it does, sign it. Do not sign the back of the money order — this is where the recipient will endorse it.

6. Keep Your Receipt

Keep the money order receipt for your records. It serves as proof of payment and allows you to track whether the money order has been cashed. Plus, you’ll need it if you want to cancel the order.

Don’t confuse the official money order receipt with any receipt you get from the issuer. It’s smart to keep both, but the official money order receipt is attached to the money order you receive. You remove it by tearing at the perforation.

Money Order Writing FAQs

Since money orders aren’t that common anymore, some questions naturally pop up about writing them.

Where Can I Get a Money Order?

You can get a money order at a business near you. Types of businesses to check include:

- Banks and credit unions

- Post offices and non-government parcel and post businesses

- Money-sending businesses like Western Union or MoneyGram

- Convenience stores, pharmacies, and big-box stores like 7-Eleven, CVS, Walmart, and K-Mart

- Grocery stores such as Safeway, Kroger, Publix, and Meijer

How Can I Pay for a Money Order?

Cash, debit card, and traveler’s checks are commonly accepted forms of payment for money orders. Some issuers also accept credit cards, but your credit card company may consider this a cash advance and charge you a fee and higher interest than it would for a purchase.

What Do I Do if I Make a Mistake Writing a Money Order?

Writing over any information on a money order invalidates it. If you make a mistake filling out a money order, such as spelling the recipient’s name wrong, you must cancel the order and write a new one with the correct information.

Can I Cancel a Money Order?

If your money order is lost or stolen, or you fill it out incorrectly, you can cancel it by contacting the issuer. You’ll need to provide the money order tracking number and complete a cancellation form.

You may also need to pay a cancellation fee, which typically ranges from $6 to $15 if you have your receipt and up to $30 if you don’t.

Can I Get a Refund if a Money Order Isn’t Cashed?

Money orders don’t have expiration dates, so you can ask for a refund anytime if the recipient doesn’t cash it. The process and fees are the same as for canceling a money order.

However, bear in mind that certain issuers begin charging fees if a money order is uncashed for a year or more. This will eat into your refund amount, so don’t wait too long if your money order hasn’t been cashed.

What’s the Difference Between a Money Order & a Cashier’s Check?

Money orders and cashier’s checks (also known as bank checks) are both guaranteed forms of payment. You pay for them upfront, so the recipient knows you’re good for the money you’re sending them.

While you can get a money order without a bank account, a cashier’s check is issued by your bank, and the money comes out of your account. Cashier’s checks typically have higher dollar amount limits than money orders, but they come with higher fees.

Final Word

A money order can be helpful if you need to send a large amount of money but don’t want to send cash, which can easily be lost or stolen. You don’t need a bank account to send one, and even if you have an account, a money order is typically cheaper than a cashier’s check.

Plus, unlike cashier’s and personal checks, money orders don’t include your bank account and routing number. This protects your sensitive personal information from ne’er-do-wells.

Consider it one more tool in your payments arsenal.

Editorial & Advertiser Disclosure: The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.

Related: