Mastercard® Gold Card™

Pros

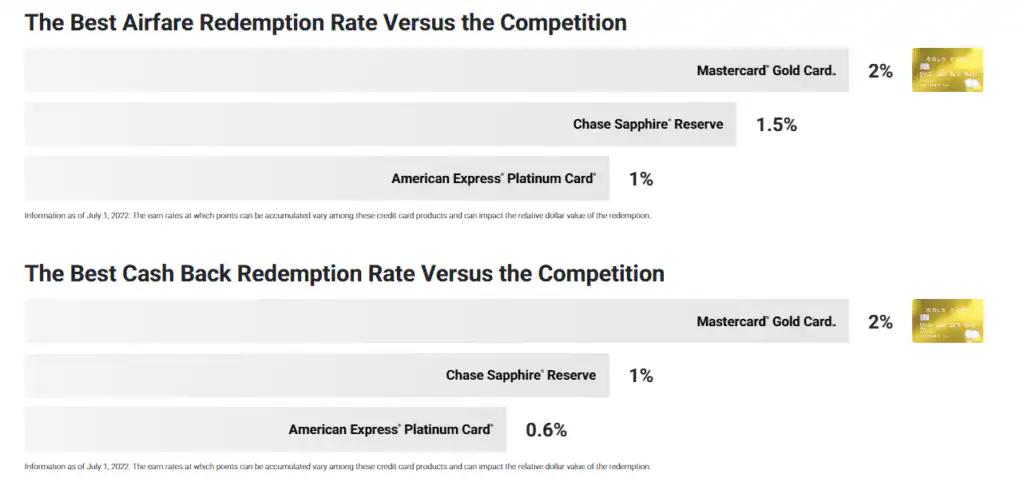

- 2% return on airfare and cash back redemptions

- $200 annual airline fee credit

- Complimentary airport lounge access (1,300+ Priority Pass Select lounges)

Cons

- $995 annual fee + $295 annual authorized user fee

- No sign-up bonus or recurring loyalty bonus

- Redemption ROI capped at 2%

The Mastercard® Gold Card™ is an extremely exclusive travel rewards credit card. And it’s expensive. The Gold Card’s $995 annual fee — and $295 annual fee per additional authorized user) — is higher than virtually any other card on the market.

Do you get what you pay for? That depends a lot on how often you travel, how much you spend, and frankly how much you invest in visible status symbols. Let’s take a look at the Gold Card’s key selling points and see how it compares to its more affordable Luxury Card™ stablemates: the Mastercard® Titanium Card™ ($195 annual fee) and the Mastercard® Black Card™ ($495 annual fee).

Is the Mastercard Gold Card Worth It?

It bears repeating: The Mastercard Gold Card has a $995 annual fee and charges $295 per year, per additional authorized user. In a two-adult household, that’s a potential annual fee of $1,290.

By contrast, other super-luxe travel cards’ annual fees top out under $700. Some, like the Capital One Venture X Rewards Card, have annual fees under $400.

Fine, but does the Mastercard Gold Card have more (and more valuable) benefits and rewards than those cards?

Let’s address the rewards program first, where the value is solid but not what you’d hope from a card with such a high annual fee.

Purchases made with the Gold Card earn 1 point for every $1 spent, with no higher earning rates on special categories, but also no restrictions or limitations on earning. Airline redemptions and cash back redemptions value points at $0.02 apiece — a 2% return on spending, doubling the value for gift card and merchandise redemptions. (Terms and conditions apply.)

On the benefits side, there’s a lot of “there” there. But again, it’s not clear that the Gold Card offers substantially more value than the American Express Platinum Card, which is far more affordable. The major highlights:

- Super-valuable benefits at more than 3,000 participating hotels and resorts worldwide worth $500 per stay (mostly high-end spots that cost many hundreds of dollars per night, if not more)

- Complimentary airport lounge access at more than 1,300 Priority Pass airport lounge locations in more than 500 cities worldwide for the cardmember and all traveling guests

- A $100 Global Entry and TSA Pre✓® application fee credit

- A $200 annual airline credit

- 24/7 concierge availability by phone, email, and live chat within the app

- Airport meet-and-greet service

- Lyft credits ($5 per month with at least 3 eligible rides during the period)

- Complimentary subscription to Shoprunner (a $79 value)

Doing the math here, it’s going to come down to how often you travel, how much you spend when you do, and the extent to which your specific travel patterns lend themselves to the open-ended benefits (specifically the hotel-and-resort perks and airport lounge access). If you make 20 airport lounge visits with a traveling companion each year and avoid the combined $120 entry fee each time, you’ll obviously come out ahead (netting $2,400 in value).

But what if you only visit three lounges per year and can’t make it to any of the participating hotels? In that case, you’ll have to spend your way out of the hole. You’ll need to spend about $50,000 on your card each year and redeem for cash back and/or airfare to earn $1,000 in rewards and clear the primary cardholder’s annual fee. Doable if your income lands you in the top 15% or 20% of U.S. households and this is your primary credit card, for sure, but not realistic for most middle-class folks.

By the way, if you’re into that sort of thing (I’m not, personally), the Gold Card is coated with real, 24-karat gold. At least it looks like a status symbol.

Key Features of the Mastercard Gold Card

Let’s dive into the details of the Mastercard Gold Card. Here’s what to expect after you’re approved.

Earning Points

The Gold Card earns 1 point for every $1 spent on all eligible purchases. Points never expire, provided your account remains open and in good standing, and there are no restrictions on the number of points you can earn.

Redeeming Points

The Gold Card has no confusing tiers, rotating categories, or redemption thresholds. You never have to wait to redeem your points, and no bank account is required for cash back redemption.

The two ideal ways to redeem points earned with your Gold Card are cash back statement credits and airfare. Both effectively offer a 2% return on your spending by valuing points at $0.02 apiece. In the case of airfare redemptions, that return comes regardless of the underlying cost of the ticket, route, carrier, or other factors. As an example, a 10,000-point redemption is worth $200 in both airfare and cash back via statement credit.

Luxury Card makes a big deal of this 2% return, and it’s true that it results in an effective return of 2% on all spending when you redeem for cash or airfare. But other high-end travel cards earn rewards at higher rates than the Gold Card — the Chase Sapphire Reserve Card earns 3x points on travel and dining purchases, resulting in an effective 4.5% return when you redeem for airfare (and other travel purchases that the Gold Card doesn’t favor). So Sapphire Reserve is actually much more lucrative than Gold if you concentrate your spending in those high-earning categories and redeem for travel.

Airport Lounge Access With Priority Pass Select Membership

The Gold Card entitles the cardmember and ticketed traveling companions to complimentary, unlimited access to about 1,300 airport lounges worldwide through Priority Pass Select, a global airport lounge network.

Priority Pass Select has lounges in more than 100 countries and 500 cities worldwide, including a few dozen restaurant lounges where Gold Card members enjoy dining discounts around $30 per visit. Lounge access is always complimentary for all guests of the cardmember, including friends that are not direct family, as long as they’re ticketed for same-day travel.

Annual Airline Credit

You receive a $200 annual airline credit every year your account remains open and in good standing. The credit can be redeemed for virtually any airline purchase, including class upgrades, baggage fees, on-board purchases, and more. The credit is automatically applied to your account as a statement credit.

TSA Pre✓® or Global Entry Fee Application Credit

Gold Card membership comes with a $100 credit toward your TSA Pre✓® or Global Entry application fee, redeemable at a time of your choosing. You’ll need to invoke this benefit at least once every 5 years to keep ahead of your membership’s expiration.

24/7 Concierge Service

The Gold Card comes with 24/7, white-glove concierge service from a dedicated cohort of professional concierges that serve only Luxury Card members. Available by phone, email, and live chat within the app (very helpful for avoiding costly international calls, these concierge services include:

- Help making restaurant or club reservations, which is especially helpful in foreign markets where apps like OpenTable are unreliable and language barriers make DIY reservations difficult

- Help with complex travel and tour bookings

- Securing tickets to events large and small

- Arranging car rental and limousine service anywhere in the world

- Arranging flower, grocery, and dry goods deliveries at home or abroad

- Inventory and pricing research for hard-to-find items

- Directions to gas stations, supermarkets, parking garages, tourist attractions, and more

Luxury Card Travel Benefits

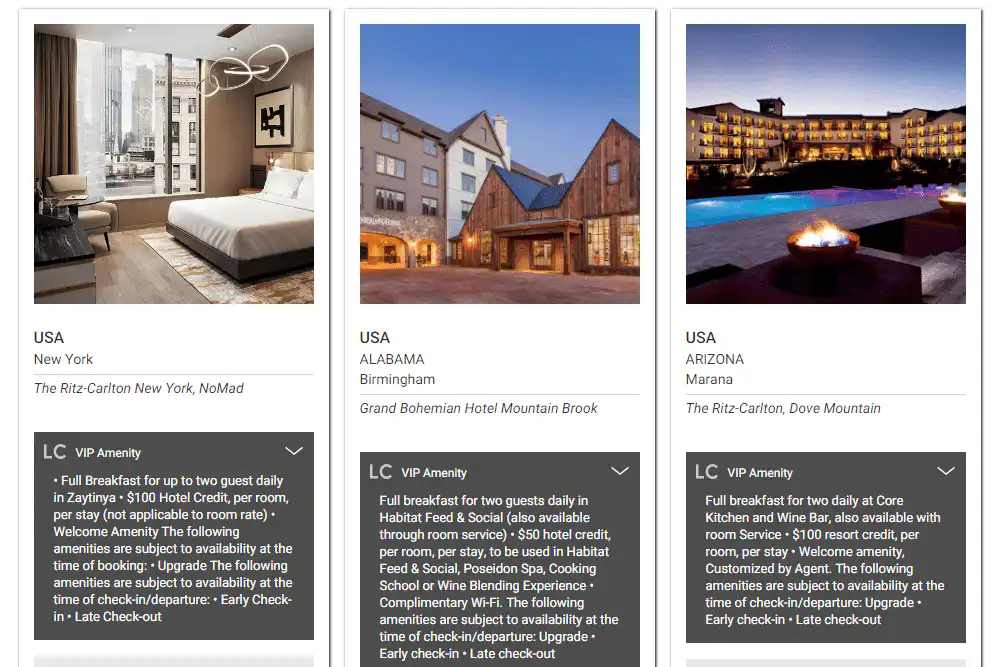

Cardmembers enjoy an average value of $500 in benefits, services, and “competitive rates” per stay at over 3,000 properties around the world, according to Luxury Card. That’s just an average: The more you stay at participating properties, the greater the value you’ll capture.

Participating brands include Montage, St. Regis, Park Hyatt, The Peninsula, Ritz Carlton, Fairmont, and more. Typical benefits include spa credits, room upgrades, complimentary food and beverages, early check-in, late check-out, and welcome gifts.

For example, a one-night stay at California Viceroy L’Ermitage Beverly Hills includes breakfast for two (a $50 value each), plus a $100 resort credit, free WiFi, and complimentary use of the hotel’s car within two miles of the resort. The similarly high-end properties below offer similar benefits (image from the Luxury Card Travel website):

Mastercard-Backed Travel Benefits

The Gold Card has a few more down-to-earth benefits backed by Mastercard, too. Many are commonly included in standard travel insurance policies, but you don’t have to pay extra for them unless explicitly indicated. The highlights:

- Baggage delay insurance, which provides reimbursement (up to specified limits) for checked baggage delayed significantly on common carrier travel.

- Travel accident insurance coverage on common carrier travel

- Complimentary rental car insurance (loss and damage waiver) when you pay the full cost of the rental on your card.

- Trip cancellation and interruption coverage, subject to limitations and exclusions.

Additional Mastercard Benefits

The Gold Card has some non-travel benefits backed by Mastercard as well. Highlights include:

- Enjoy complimentary cell phone protection up to $800 per claim and $1,000 per covered card in a 12-month period (maximum two claims). Each claim is subject to a $25 deductible.

- Take at least 3 eligible Lyft rides per month using your Gold Card to earn a $5 Lyft credit.

- Receive 2-day free shipping and free return shipping on eligible purchases when you sign up for a complimentary ShopRunner membership using your Gold Card.

Another key Mastercard benefit, Mastercard ID Theft Protection, features monitoring on the covered cardmember’s:

- Email addresses

- Debit/credit cards/prepaid cards

- Bank accounts

- Web logins (username and password)

- Medical insurance cards

- Driver’s license

- Loyalty cards

- Affinity cards

- Passport number

- Vehicle insurance cards

- Social Security number

Priceless Events

Gold Card users get special (and occasionally members-only) access to Mastercard’s ever-shifting lineup of “Priceless” events and experiences. “Priceless” events are frequently invite-only or limited to VIPs (including high-end Mastercard members). Events can include hot tickets such as VIP access at pro golf tournaments, private dinners with award-winning chefs, and curated city experiences in exotic places such as Dubai. Additional fees and expenses, such as airfare, may apply.

Magazine Subscription

All Luxury Card members, including Gold Card holders, get complimentary subscriptions to LUXURY MAGAZINE, Luxury Card’s bi-annual glossy mag whose content caters to an affluent readership and covers such topics as technology, architecture, real estate, autos, and travel.

Important Fees

This card has a $995 annual fee that is not waived in the first year. Each additional authorized user costs $295 per year. There is no foreign transaction fee.

Credit Required

This card requires excellent credit. Any notable issues in your credit history are likely to disqualify your application.

APR

This card offers an Ongoing Purchase APR that may be 21.24%, 25.43% or 28.24%, depending on the cardholder’s creditworthiness. Additionally, the card has a Cash Advance APR of 30.49%, which will vary with the market based on the Prime Rate.

Balance Transfers

This card features a 0% introductory APR on balance transfers that post within 45 days of account opening, lasting for the first fifteen billing cycles. This provides a valuable opportunity to pay off transferred debt without interest. However, the APR will be 21.24%, 25.43% or 28.24% after this period or for transfers outside the 45-day window, based on creditworthiness. Additionally, a fee of either $5 or 5% of the amount of each transfer, whichever is greater, will be applied.

Advantages of the Mastercard Gold Card

Clearly, the Mastercard Gold Card has a lot going for it. Whether it’s worth the eye-watering cost is another question, but let’s review its core advantages anyway.

- Airfare Redemptions Double Regular Point Values. The Gold Card values points at $0.02 apiece when redeemed for airfare, regardless of the demand, dollar cost, destination, carrier, or other factors that frequently affect airfare redemption values. Though $0.02 per point is not a stellar valuation, it’s better than the typical value offered by major carriers for domestic flights, and its predictability (always $0.02 per point, no matter what) makes it easier to plan ahead for redemptions.

- Cash Back Redemptions Exceed Expectations. Cash back redemptions also provide a 2% return on all spending – turning a 10,000-point redemption into a $200 statement credit, for example. By comparison, the vast majority of traditional cash back credit cards value points at $0.01 apiece. If you spend very heavily throughout the year, you can make significant progress toward offsetting this card’s annual fee – for instance, $50,000 in annual spending equates to $1,000 cash back, no matter what you spend on.

- High-Touch Concierge Service. Cardmembers enjoy 24/7 service from dedicated concierges available by phone, SMS, email, and live chat within the app. They can help with everything from dinner and transportation reservations in unfamiliar international markets to snagging hard-to-find supplies closer to home. For travelers abroad, concierge access through the app can significantly reduce the cost of international phone calls.

- Complimentary Airport Lounge Access at 1,300+ Priority Pass Select Locations. Gold Card users get complimentary access to more than 1,300 airport lounges in approximately 500 major destinations around the world. It’s easier to find Priority Pass lounges than branded lounges operated by big U.S. carriers, such as Alaska Airlines, Delta, and United, so this membership is definitely a better deal than, say, Delta Sky Club or United Club. If you’re able to use your Priority Pass membership every time you travel (or nearly so), this benefit can make a big dent in the Gold Card’s annual fee.

- Very Generous Travel Benefits. The Gold Card has some other valuable travel benefits, notably the $200 annual airline credit and the $100 Global Entry application fee credit. Some other benefits don’t have fixed dollar values, but are nonetheless useful. Taken together and exploited to the fullest along with the airport lounge benefit, they can more than offset the Gold Card’s recurring fee.

- No Foreign Transaction Fee. The Gold Card never charges foreign transaction fees, making it a great choice for frequent international travelers.

Disadvantages of the Mastercard Gold Card

For a supposedly generous travel card, the Mastercard Gold Card has some significant drawbacks. And the less you spend on your card each year, the more glaring these downsides become.

- Extremely High Annual and Authorized User Fees. At $995, the Gold Card’s annual fee is higher than just about any other travel card on the market. For couples and families, the $295 annual authorized user fee adds to the expense. These fees are prohibitive for the vast majority of the card-holding public, including anyone who doesn’t travel with predictable frequency. If you can’t fully exploit the Gold Card’s considerable travel benefits or spend heavily enough ($50,000 or more per year) to offset the annual fee, this is not your card.

- Low, Flat Point Earning Rate on All Purchases. All Gold Card purchases earn unlimited 1 point per $1 spent – the standard base rate for most travel and cash back rewards credit cards. While not awful, this rate is decidedly mediocre, and there’s no way to accelerate your earnings above and beyond it. This means that the highest possible rate of return on spending with the Gold Card is 2% – pretty good, but not amazing, especially in light of the hefty annual fee. Compare the Gold Card’s earning rate with that of Citi ThankYou Premier, which earns 3 points per $1 spent on travel and 2 points per $1 spent on dining and entertainment.

- No Sign-up Bonus. The Gold Card has no sign-up bonus, a curious omission for a travel card. For a potentially generous sign-up bonus, look to the Platinum Card from American Express.

- No Recurring Loyalty Bonus. The Gold Card also has no annual loyalty bonus. That’s unusual among exclusive airline and hotel credit cards, which frequently offer free or discounted flights and nights – or enough bonus points to reduce or eliminate the cost of a flight or stay – on cardmembers’ sign-up anniversaries. Some exclusive travel cards go even further – for example, Citi Prestige cardholders automatically get the 4th night free on stays of 4 nights or longer, up to 2 per year.

- Travel Credit Isn’t as Generous as Some Competing Cards. The Gold Card’s $200 annual airline credit certainly helps around the margins. However, it’s not world-beating, especially in light of the Gold Card’s excessive annual fee. Citi Prestige, another exclusive option, has a $250 annual air travel credit.

How the Mastercard Gold Card Stacks Up

Should you go ahead and apply for the Mastercard Gold Card, or is one of the other two Luxury Cards more your speed? See how they compare:

| Gold Card | Black Card | Titanium Card | |

| Annual Fee | $995 | $495 | $195 |

| Authorized User Fee | $295 | $195 | $95 |

| Cash Value | 2% | 1.5% | 1% |

| Airfare Value | 2% | 2% | 2% |

| Airline Fee Credit | $200/year | $100/year | None |

| Priority Pass | Yes | Yes | No |

| Intro Balance Transfer APR | 0% | 0% | 0% |

| Ongoing APR | 21.24%, 25.43% or 28.24% | 21.24%, 25.43% or 28.24% | 21.24%, 25.43%, or 28.24% |

Final Word

The Mastercard® Gold Card™ is quite unlike any other credit card on the market. For starters, there’s the small matter of its 24-karat gold exterior – a marker of exclusivity if there ever was one. On more practical measures, the Gold Card is no less unusual. It values cash back points at $0.02 apiece, double the standard for regular cash back credit cards, though the mediocre point-earning rate blunts the impact.

On other measures, the Gold Card looks more traditional. It has an extensive but not groundbreaking lineup of VIP travel benefits designed to reduce the stress, inconvenience, and expense associated with frequent travel. If you’re a committed road warrior who doesn’t have time to follow the herd, the Gold Card could be worth it. Otherwise, consider the more economical Mastercard Black Card or Mastercard Titanium Card.

Editorial & Advertiser Disclosure: The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.

Related: