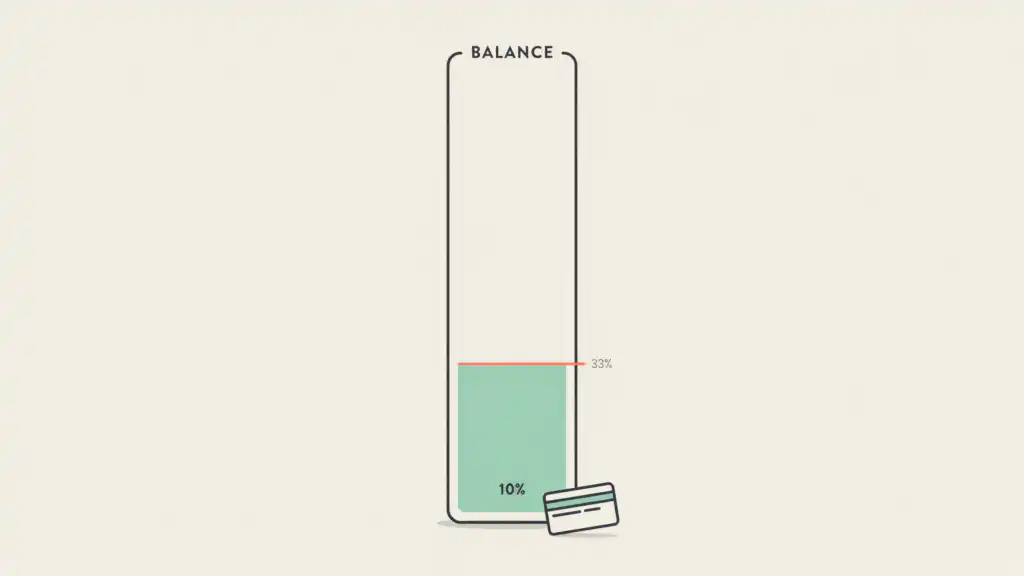

Your Credit Utilization Should Stay Below 30% – Ideally Below 10%

Credit utilization is the percentage of your available credit you’re using, and it’s the second biggest factor in your credit score. Keeping it below 30% is standard advice, but the highest scores cluster below 10%. If you carry balances, pay them down before your statement closes, not just before the due date.