Credit One Bank® Platinum Visa® for Rebuilding Credit

Pros

- No security deposit required

- Earn up to 10% cash back

- Qualify with below-average credit

Cons

- Has an annual fee ($75 the first year, $99 thereafter)

- No sign-up bonus

- Low maximum credit limit

The Credit One Bank® Platinum Visa® for Rebuilding Credit is an unsecured, entry-level credit card for cardholders seeking to rebuild their credit and put their financial lives back on track. Its annual fee is $75 for the first year and $99 each year thereafter, billed at $8.25 per month.

The credit limit ranges up to $1,500, with no initial or ongoing security deposits required.

This is not a generous credit card by any means. It has no sign-up bonus, no real cardholder benefits to speak of, a fairly low credit limit, and potentially pricey cash advances. But it does have a decent cash-back program that earns 1% back on eligible purchases, and purchases with select merchants earn even more — up to 10% back.

Plus, Credit One’s lenient underwriting standards mean that for cardholders with average or even below-average credit, Credit One Bank Platinum Visa for Rebuilding Credit is likely to be one of the few available options that requires no security deposit. That’s an important point of distinction if you’re on a tight personal budget and can’t cough up the cash for a security deposit right now.

How the Credit One Bank® Platinum Visa® for Rebuilding Credit Stacks Up

The Credit One Bank Platinum Visa for Rebuilding Credit isn’t the only entry-level credit card for people with less-than-perfect credit scores. Let’s see how it stacks up against another unsecured card for folks looking to get their credit back on track: the Capital One® QuicksilverOne® Cash Rewards Credit Card.

| Credit One Platinum Visa | Capital One QuicksilverOne | |

| Annual Fee | $75 for the first year, then $99/year | $39 |

| Rewards | 1% cash back on select purchases, up to 10% back with eligible merchants | 1.5% cash back on all eligible purchases |

| Credit Limit | $300 minimum, $1,500 maximum | $300 minimum, variable maximum |

| Automatic Credit Limit Increases | Yes | Yes |

Key Features of the Credit One Bank Platinum Visa for Rebuilding Credit

Interested? Here’s what you need to know about the Credit One Bank Platinum Visa for Rebuilding Credit.

Credit Limit

This card carries a minimum credit limit of $300 and a maximum credit limit of $1,500.

You can’t charge more than $1,500 without paying off some or all of your preexisting balance. It takes up to 12 days for balance payments to reduce your credit limit.

Credit Limit Increase

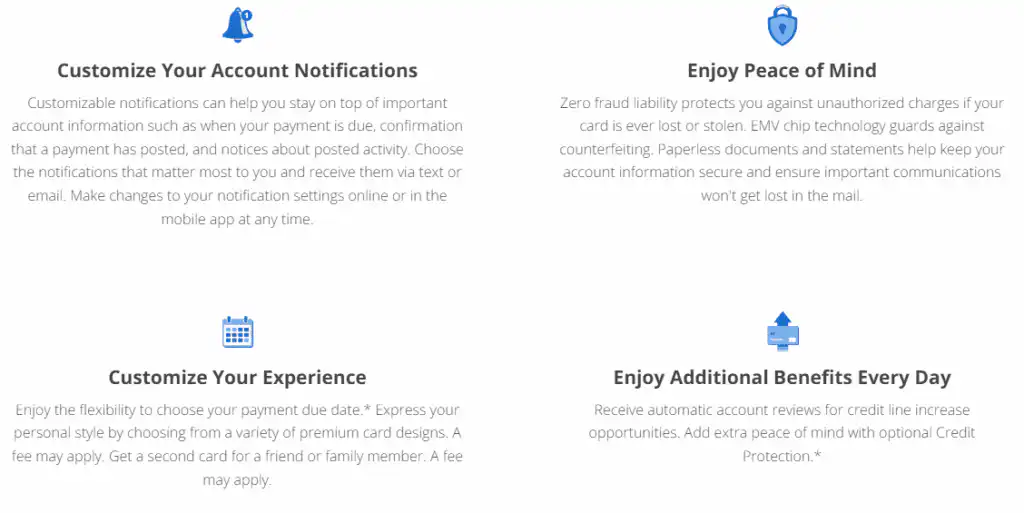

Credit One reviews your account regularly for credit line increase opportunities and promptly ups your credit when it feels you deserve it.

Earning Cash Back Rewards

Earn 1% cash back on eligible net purchases of gas, groceries, mobile phone, Internet, cable, and satellite TV services. Select purchases with eligible merchants earn up to 10% cash back.

Redeeming Cash Back Rewards

Each month’s cash back automatically posts to your credit card account as a statement credit. There’s no minimum redemption threshold and no action required on your part.

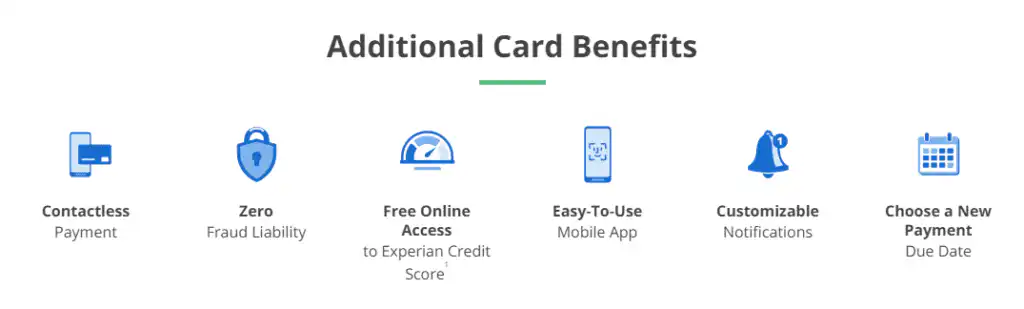

Free FICO Score Each Month

Every month, Credit One Bank provides you with an updated FICO score on your account statement. Your score is also visible in your online account dashboard. There’s no fee to see it.

Important Fees

Credit One Bank Platinum Visa’s annual fee is $75 during the first year your account is open. In all subsequent years, it’s $99, billed $8.25 monthly.

Cash advances cost the greater of $5 or 8% of the transferred amount. The foreign transaction fee is the greater of $1 or 3%. Other fees may apply.

Credit Required

This card has very permissive credit standards, and it’s likely that applicants with average or even below-average credit will qualify. However, very serious issues in your recent credit history, including bankruptcies and foreclosures, are likely to disqualify your application.

Advantages of the Credit One Bank Platinum Visa for Rebuilding Credit

The Credit One Bank Platinum Visa for Rebuilding Credit packs an impressive punch for a credit-rebuilding card. These are its top advantages.

- No Security Deposit Required. Unlike many cards designed for credit-challenged cardholders, Credit One Bank Platinum Visa for Rebuilding Credit is not secured and therefore doesn’t require new cardholders to make upfront security deposits. Some popular secured credit cards require at least $200 or $300 upfront before activating cardholders’ accounts, followed by additional deposits whenever cardholders wish to raise their credit limits. For many cash-strapped consumers intent on improving their credit, that’s a tall order.

- Decent Rewards for Its Category. Credit One Bank Unsecured Visa’s maximum 1% cash back rate on everyday purchases isn’t spectacular by premium cash back card standards, but it’s not bad at all for cash back cards built for consumers with below average credit. If you’re looking to rebuild credit and earn a return on spending, you’d do worse than this card. And the promise of 10% cash back on select purchases sweetens the deal even further.

- No Penalty APR. Credit One Bank Platinum Visa doesn’t charge penalty interest. That’s a potential lifesaver for cardholders who occasionally miss payments due to liquidity issues. Some secured and entry-level credit-building cards charge penalty interest at rates as high as 30% on an indefinite basis. That can significantly add to the cost of carried balances.

- Free Credit Score Each Month. You get a free FICO score with your monthly statement and in your online account dashboard. This allows you to track changes in your credit at a glance and make connections between your credit score and your spending, credit utilization, balance payments, and other activities.

- Permissive Qualification Standards. By non-secured card standards, Credit One Bank Unsecured Visa is very easy to obtain. If you have average or even below-average credit, it’s worth your while to apply for this card. While approval is never guaranteed, it’s far more likely that you’ll be approved for this card at a low credit limit than for a more generous cash back card at any terms. This can be a great first step on the road to better credit.

- Responsible Use Builds Credit Over Time and Could Increase Your Credit Limit. Credit One Bank reports your payment patterns and credit utilization habits to all three major credit reporting bureaus each month. If you use this card responsibly and make timely payments, this is likely to improve your credit over time, hopefully paving the way for a more generous credit card in the near future. Plus, Credit One regularly monitors your account usage and taps you for a credit limit increase after you’ve consistently demonstrated responsible use.

Disadvantages of the Credit One Bank Platinum Visa for Rebuilding Credit

The Credit One Bank Platinum Visa for Rebuilding Credit has some notable disadvantages, including an unavoidable annual fee, low credit limit, and no sign-up bonus.

- Has an Annual Fee. The Credit One Bank Platinum Visa for Rebuilding Credit has a $75 annual fee in the first year and a $99 annual fee each year thereafter, though the $8.25 monthly charge lessens the sting a bit.

- No Sign-up Bonus. This card doesn’t have a sign-up bonus. That’s a big problem for applicants looking to juice their earnings right out of the gate. If you’re looking for an entry-level cash back card with a decent early spend bonus, check out the Capital One Quicksilver Cash Rewards Credit Card or the Chase Freedom Credit Card.

- Low Maximum Credit Limit. This card’s maximum credit limit is $1,500. If you intend to use Credit One Bank Unsecured Visa as your family’s everyday spending card, that may be too low, unless your cash flow is sufficient to pay off purchases as you make them. Some competing secured cards have spending limits as high as $5,000 or $10,000. Those levels are much more comfortable for moderate to heavy spenders.

- No Balance Transfers. You can’t make balance transfers to the Credit One Bank Platinum Visa for Rebuilding Credit. If you’re facing high-interest balances on an existing credit card account, look to a tried-and-true balance transfer card such as Chase Slate Edge or Citi Simplicity (though be aware that both require good credit).

- Potentially High Cash Advance Fees. Credit One Bank Platinum Visa’s cash advances can cost as much as 8% of the advanced amount. Most other cards cap cash advance fees at 5% of the advanced amount, so that’s a big (and potentially costly) difference.

Final Word

The Credit One Bank® Platinum Visa® for Rebuilding Credit is not an aspirational credit card. In fact, as credit cards go, it’s pretty unremarkable. However, for consumers who’ve struggled with credit issues in the relatively recent past and find that most of their credit card options require a hefty upfront security deposit, it’s a valuable alternative. If you struggle to qualify for more generous cards, give Credit One Bank Unsecured Visa a try. With responsible credit utilization and timely balance payments, you could find move up in the credit card world a lot sooner than you imagine.

Editorial & Advertiser Disclosure: The editorial content on this page is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed here are ours alone, not those of any advertiser. The offers that appear on this site are from companies that compensate us. That compensation may influence which products we cover and where and how they appear on a page – including the order in which they appear – but it does not influence our evaluations, ratings, or opinions. We do not include every company or offer available in the marketplace.

Related: