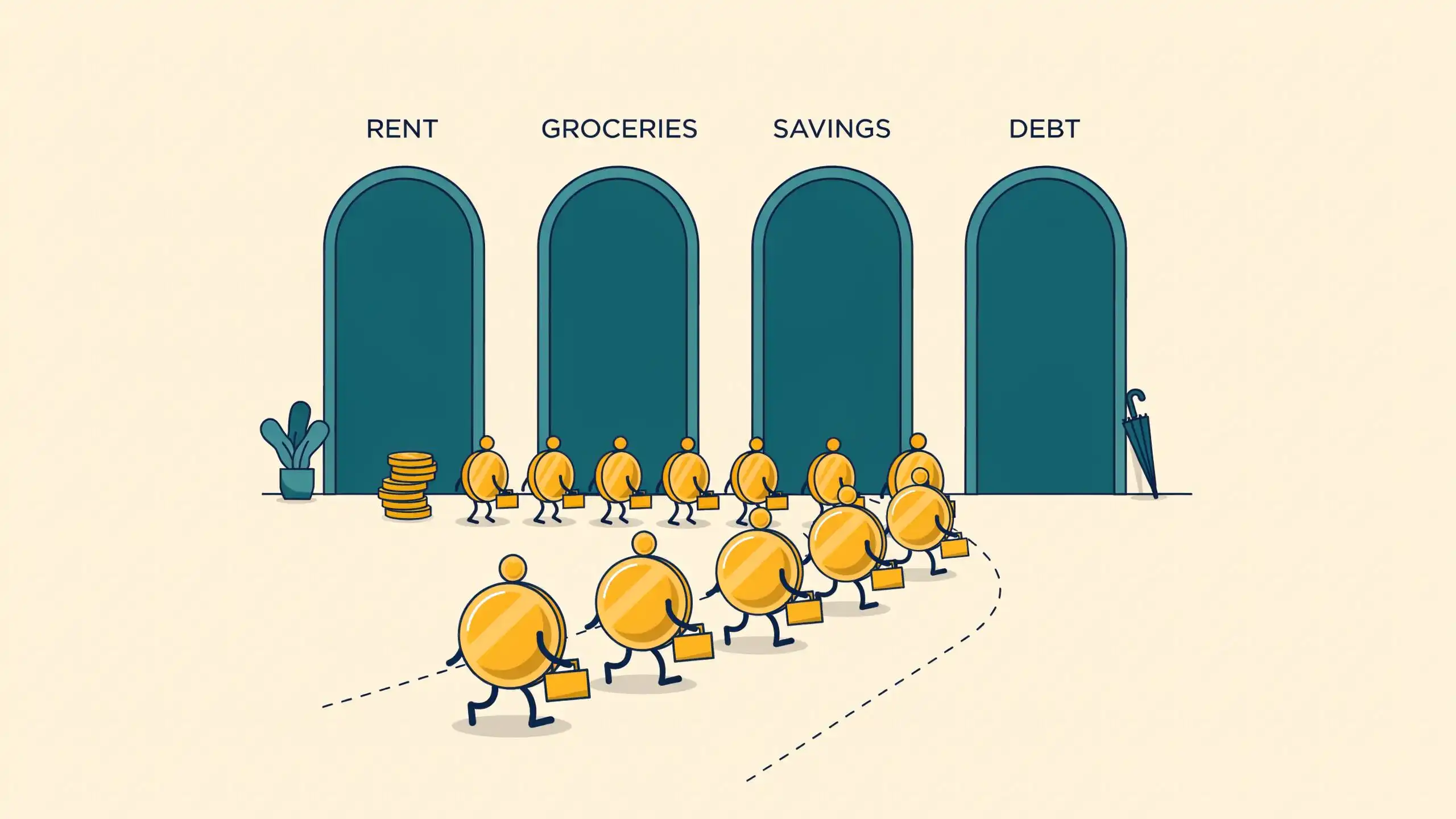

Zero-based budgeting means allocating every dollar of your income to a specific category until you reach zero. You’re not spending it all. You’re assigning it all, and savings, investments, and debt payments are categories just like rent and groceries. Give every dollar a destination before the month starts and money stops disappearing without explanation.

Most budgets only make decisions about some of your money. Bills get planned, savings might get a number, and everything else floats in a loose pool of whatever’s left. That pool is where overspending lives.

Zero-based budgeting closes the loophole. Your income minus your assignments equals zero, so no dollar sits around waiting to be spent by default. The unassigned $200 you meant to save quietly becomes takeout, an extra subscription, and a sale you didn’t plan for.

The order of operations is the real shift. Instead of spending first and saving whatever survives, you decide everything up front. “Save what’s left” fails for most people because nothing is ever left. When you fund savings and debt payments on day one, they stop competing with impulse purchases for scraps.

Start before the month does. Write down your expected take-home pay, then list every category you spend in: housing, utilities, groceries, transportation, debt payments, savings, investments, and a realistic line for fun. Assign dollars to each category until your income hits zero. Add a small miscellaneous category so a surprise expense doesn’t wreck the plan. If you’re paid every two weeks, build the month from two paychecks and assign each one as it lands.

Then track as the month unfolds. When groceries run over, move money from another category to cover it. Reassigning mid-month is how the system works, not a sign you failed. A notebook or spreadsheet handles the math fine, and several budgeting apps are built entirely around the method if you’d rather automate it.

A dollar without a job finds one on its own, and it rarely picks the job you’d want. Assign all of them before the month starts, and every dollar works on something you chose.

Editorial & Advertiser Disclosure: The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.

Related: