One of the main reasons to invest your money is to make more of it by earning interest and dividends.

You earn interest from loaning your money to banks in the form of savings accounts, certificates of deposit, bonds, or peer-to-peer loans. You earn dividends by investing in stocks or private businesses.

But that income isn’t free. You have to pay taxes on it. That’s where IRS Schedule B comes in.

What Is IRS Schedule B?

IRS Schedule B is the tax form used to report interest and dividend income, but you might not need to use it, even if you have these types of income.

You only need to complete Schedule B and attach it to your Form 1040 if one of the following situations applies:

- You received more than $1,500 of taxable interest or dividend income during the tax year.

- You received interest from a seller-financed mortgage and the buyer used the property as their personal residence.

- You have accrued interest income from a bond. This happens when you buy a bond between interest payment dates and pay the accrued interest to the seller.

- You need to report original issue discount (OID) income that is less than the amount shown on Form 1099-OID. OID is a special type of interest that’s most common when someone buys a bond for less than its face value. The difference between the face value and purchase price of a bond is its OID.

- You need to reduce your interest income from a bond by the amount of amortizable bond premium. A bond premium occurs when you buy a bond for more than its face value. The amortizable bond premium is the amount you paid above the bond’s face value.

- You are claiming the exclusion of interest from series EE or I U.S. savings bonds issued after 1989. Check out the instructions included with Form 8815 for the rules for deducting this interest.

- You received interest or ordinary dividends as a nominee. This happens when the account is in your name, but the income actually belongs to someone else.

- You had a financial interest in, or signature authority over, a financial account in a foreign country or were involved in a foreign trust.

If none of the above situations apply, you can simply report your interest and dividend income directly on lines 2 and 3 of Form 1040.

How to Complete the Schedule B Tax Form

Taking up just one side of a single page, Schedule B is relatively simple as tax forms go. The IRS Instructions for Schedule B provide line-by-line instructions for completing this form.

However, these user-friendly instructions should help you get started.

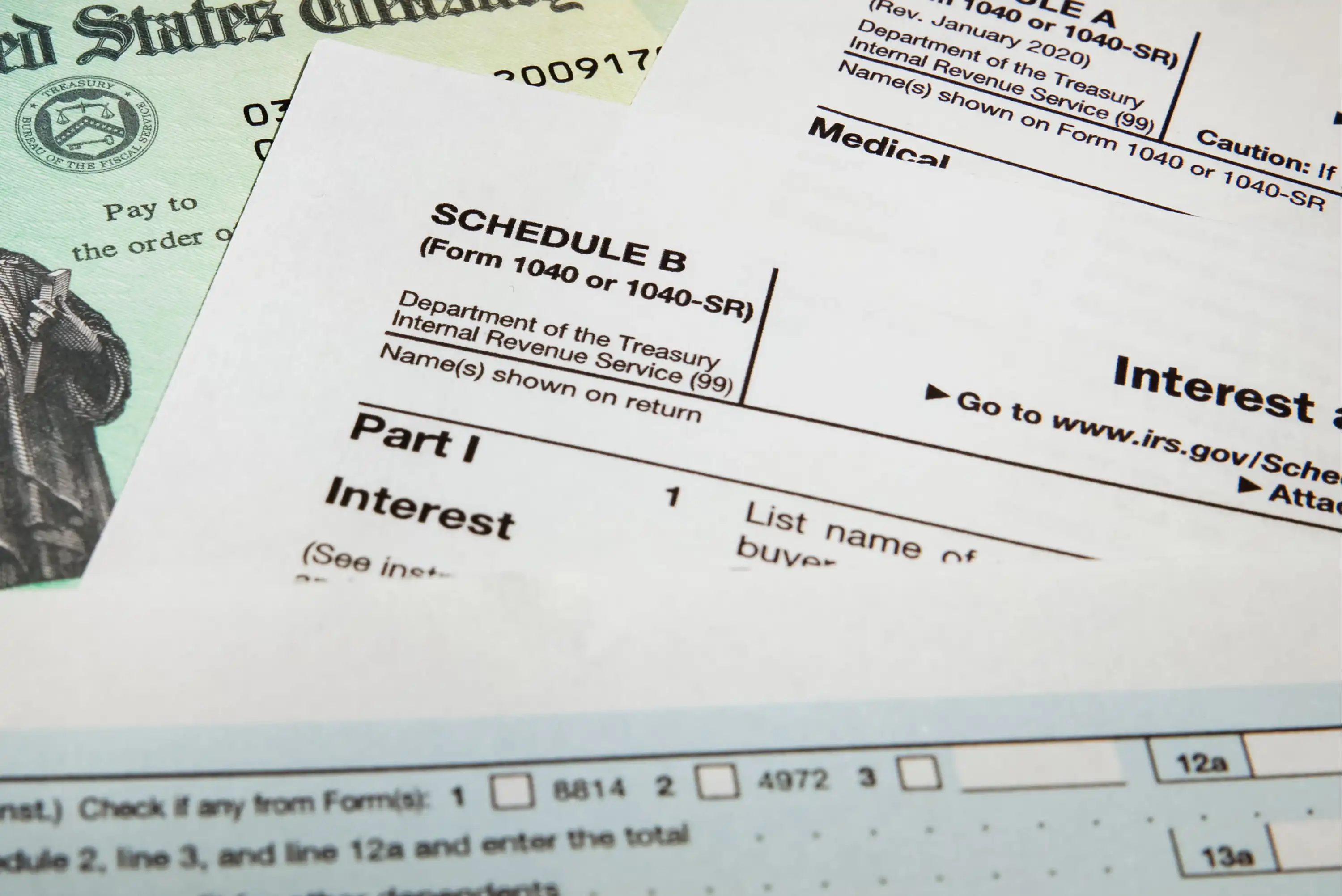

Part I

Part I of Schedule B is where you report interest income. Simply list the name of the payee on the left side of line 1, and the amount of interest income received on the right. If your 1099-INT includes both taxable and tax-exempt interest (line 8 of Form 1099-INT), enter the total on line 1.

There are 14 lines for listing each payee. If you need more room, you can attach a statement to your return listing additional payees.

Total the amounts received from all payees on line 2.

On line 3, enter the amount of tax-exempt interest, subtract line 3 from line 2, and enter the result on Line 4.

Then enter your total tax-exempt and taxable interest on lines 2a and 2b of Form 1040.

Part II

Part II of Schedule B is where you report dividend income. Like Part I, you’ll enter the payee’s name on the left and total ordinary dividends (line 1a of Form 1099-DIV) on the right. Enter the total on line 6 of this form and line 3b of Form 1040.

You can attach an additional statement listing more payees if you need to — just remember to enter the total in Part II.

If you have any qualified dividends (line 1b of Form 1099-DIV), you need to enter the total on line 3a of Form 1040.

Part III

You only need to complete Part III if you:

- Had more than $1,500 of taxable interest or ordinary dividends

- Have an interest in, or signature authority over, a foreign bank account

- Were involved in a foreign trust

Part III consists of just three yes-or-no questions, which essentially boil down to:

- Did you have a foreign account during the calendar year?

- If you did have a foreign account, are you required to file FinCen Form 114? (See FinCEN Form 114 and its instructions at www.fincen.gov to determine whether you need to file the form.)

- Were you involved in a foreign trust during the calendar year?

If you answer yes to questions 2 or 3, the IRS will expect to also receive FinCen Form 114 or Form 3520.

Final Word

Schedule B is a pretty simple form, but make no mistake: it’s important — especially for taxpayers with foreign bank accounts or trusts.

If you’re required to file Schedule B but don’t attach it to your tax return, the IRS may reject your tax return, and you may have to pay penalties and interest.

If you have any questions, make sure you reach out to a qualified tax professional through a company like H&R Block.

Editorial & Advertiser Disclosure: The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.

Related: